Reading a payslip can often be complex due to the amount of information it contains. This guide aims to help you better understand its content and how it works.

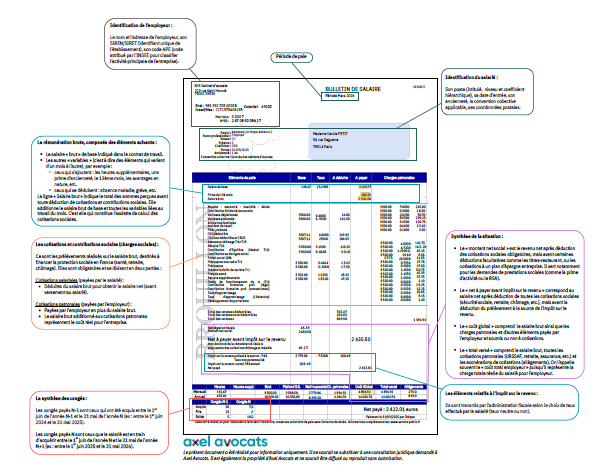

Employee and employer identification

In this section, you will find :

- The employer's name and address, their SIREN/SIRET ( unique establishment identifier ), their APE code ( code assigned by INSEE to classify the company's main activity) , and the name of the collective agreement applied in the company (a set of rules that supplement or replace the provisions of the Labor Code and are specific to the company's sector of activity. In the absence of a collective agreement, reference to the Labor Code is provided) ;

- The employee's registration number (if applicable), their social security number and the period of the payslip (the month) ;

- The employee's contact details (name, surname, postal address) ;

- The employee's position (including title and conventional classification);

- The type of contract or duration of work, the date of entry into the company, and seniority.

Components of gross remuneration

This category generally includes all sums that are considered wages and are subject to social contributions. Specifically, it includes :

- The basic "gross" salary specified in the employment contract ;

- Other "variable" elements (which vary from month to month) may be added, such as overtime, seniority bonus, 13th month, benefits in kind, etc.

There are several types of variable elements:

| Those that are added |

Those that are deducted |

- Hours at normal rate 100%

- Overtime at 125% or 150%

- Hours worked on Sundays

- Company car

- Potential bonuses

- Paid leave allowances, etc.

|

- Mostly all absences

- Unjustified absence

- Strike absence

- Lay-off absence

- Authorized unpaid absence

- Parental leave absence

- Paid leaves, etc.

|

The "Salaire brut” (Gross salary) line indicates the total amount received, before any deduction of social security contributions. It consists of the gross basis salary and all variables related to work and absences during the month.

Click on the image to download the PDF

Social security contributions and levies

These are deductions taken from gross salary, intended to finance social protection in France (health, retirement, unemployment). Social security contributions (also called "social charges") are mandatory and are divided into two parts:

Employee contributions (employee share) :

- Paid by the employee;

- Deducted from gross salary to obtain net salary (before payment to the employee).

Employer contributions (employer's share) :

- Paid by the employer in addition to the gross salary ;

- They do not appear in the net salary, but they represent a real cost to the company.

Amounts not subject to contributions are shown "at the bottom of the payslip" :

These are the amounts that are generally exempt from social security contributions, and which appear below the social security contributions, in particular:

- Meal vouchers ;

- Home-office allowance ;

- Transportation allowance ;

- Reimbursement of daily Social Security allowances (IJSS paid by the CPAM in case of work-related accident leave) ;

- Bonus on value sharing (Prime de Partage de la Valeur - PPV) ;

- Incentive bonus ;

- Participation bonus, etc.

Details of the pay period

Sometimes, the payslip specifies the pay period and the events of the month.

In this case, several elements most often appear:

- The daily calendar of the pay period with all the days counted in that period ;

- An "incident" column which includes the number of hours corresponding to a daily event, and the acronym of this daily event.

Summary of the situation

In this section, you will find :

- The "net social amount" (montant net social) : net income after deduction of mandatory social security contributions, but prior to certain optional deductions such as meal vouchers, health insurance, or employee savings plan. It is notably used for social benefits applications (such as the activity bonus – prime d’activité - or the RSA) ;

- The "net pay before income tax" (net à payer avant impôt sur le revenu) : net salary after deduction of all social contributions (social security, retirement, unemployment, etc.), but before deduction of withholding income tax ;

- The "total paid by the employer" (total versé employeur) : cumulative gross salary for the current month since the beginning of the year. It includes the gross salary and all employer contributions (URSSAF, pension, insurance, etc.). It is often called the "total employer cost" since it represents the total cost of the employee for the employer ;

- Gross taxable income (brut fiscal): the basis for calculating income tax withheld for the current month, and since the beginning of the year. It includes gross salary, minus certain exemptions or non-taxable benefits (e.g., transport reimbursement), plus certain taxable benefits (e.g., accommodation allowance, vehicle allowance). It is only used to calculate the monthly withholding tax.

- Net taxable amount (net fiscal): the actual taxable amount that the employer declares to the tax authorities to calculate income tax, for the current month and since the beginning of the year.

Summary of leave

In this section, you will find :

Paid leave N-1 for the leaves acquired between June 1 of year N-1 and May 31 of year N (ex: between June 1 , 2024 and May 31, 2025) ;

Paid leave N for the leaves acquired between June 1 of year N and May 31 of year N+1 (ex: between June 1 , 2025 and May 31, 2026).